Mortgage Blog

Get the mortgage you deserve

Is Toronto Experiencing a Real Estate Bubble?

October 31, 2018 | Posted by: Calum Ross

It’s not exactly news that ordinary Canadians are being squeezed out of many real estate markets. Prices for both single-family homes and condominiums in markets like Vancouver, Montreal and Toronto (and their suburbs) have skyrocketed — far outstripping wage growth. But developers are still building — creating more and more homes for a rapidly narrowing market of qualified buyers. On a debt-to-income basis, Toronto mortgages are in much better shape than our friends in Vancouver. But neither market is in a good spot from a household economics perspective.

The situation has caused many market observers to raise the bubble alarm.

The UBS Group Global Real Estate Bubble Index lists the major metropolitan housing markets it deems most overvalued and most at risk of proving to be asset bubbles. Canada’s own Toronto market ranks as the third most inflated housing market on the planet followed closely in fourth place by Vancouver, and both well ahead of high-priced markets like London, Paris, San Francisco, Los Angeles, Tokyo and New York. Only Hong Kong and Munich scored higher, and both classified as “bubbles” by the UBS’s analysts.

Things were even worse last year when Toronto ranked number one on the UBS Housing Bubble Index.

The United States was hit by a severe collapse in real estate prices and a massive round of mortgage defaults and foreclosures in the late 2000s. The Canadian market was spared the worst of this downturn because, unlike the U.S., housing policy in Canada does not prioritize broad increases in homeownership rates as a central goal of public policy. For example, Canada’s bank regulators do not pressure banks to issue subprime mortgages to individuals with shaky credit histories to the same extent American regulators did prior to the 2008/2009 U.S. housing market collapse.

As a result, when U.S. defaults rose to 5 percent of the total mortgage market during the bubble (and 20 percent of all sub-primes), Canadian mortgage default rates never rose above ½ of 1 percent.

But the next bear market in real estate could go a lot worse for Canadian homeowners. Here’s why:

Canada’s Household Debt Problem

Canadian consumers typically carry higher debt loads than Americans, exclusive of mortgage debt. In fact, Canada’s household debt burden is the highest of any country in the world, according to the Organization for Economic Cooperation and Development, with the household debt to GDP ratio over 100 percent.

The OECD attributes Canadian households’ status as the most indebted in the world to the inflation of real estate prices. High debt levels tend to increase the risk and severity of a recession and leave Canadian consumers in a precarious place, with little capacity to adjust to economic shocks – like a general rise in interest rates.

Unlike Americans, who usually buy homes with a 30-year fixed-rate mortgage, Canadians typically buy homes with a five year fixed rate or variable rate mortgage that has a balloon payment (the remaining mortgage debt) due at the end of five years – which means Canadian homebuyers are much more exposed to interest rate risk.

Interest rates are now beginning to climb in both the United States and Canada. Meanwhile, major Canadian housing markets are already seeing a noticeable pullback since the beginning of the year, with the Greater Toronto area leading the decline.

What is a bubble?

Yale professor Robert J. Shiller (who I read a lot of) and author of the widely-read book Irrational Exuberance, advanced a workable definition emphasizing investor psychology. According to Shiller, a bubble is “a situation in which news of price increases spurs investor enthusiasm, which spreads by psychological contagion from person to person, in the process amplifying stories that might justify the price increases and bringing in a larger and larger class of investors … despite doubts about the real value of an investment.’

How do bubbles happen?

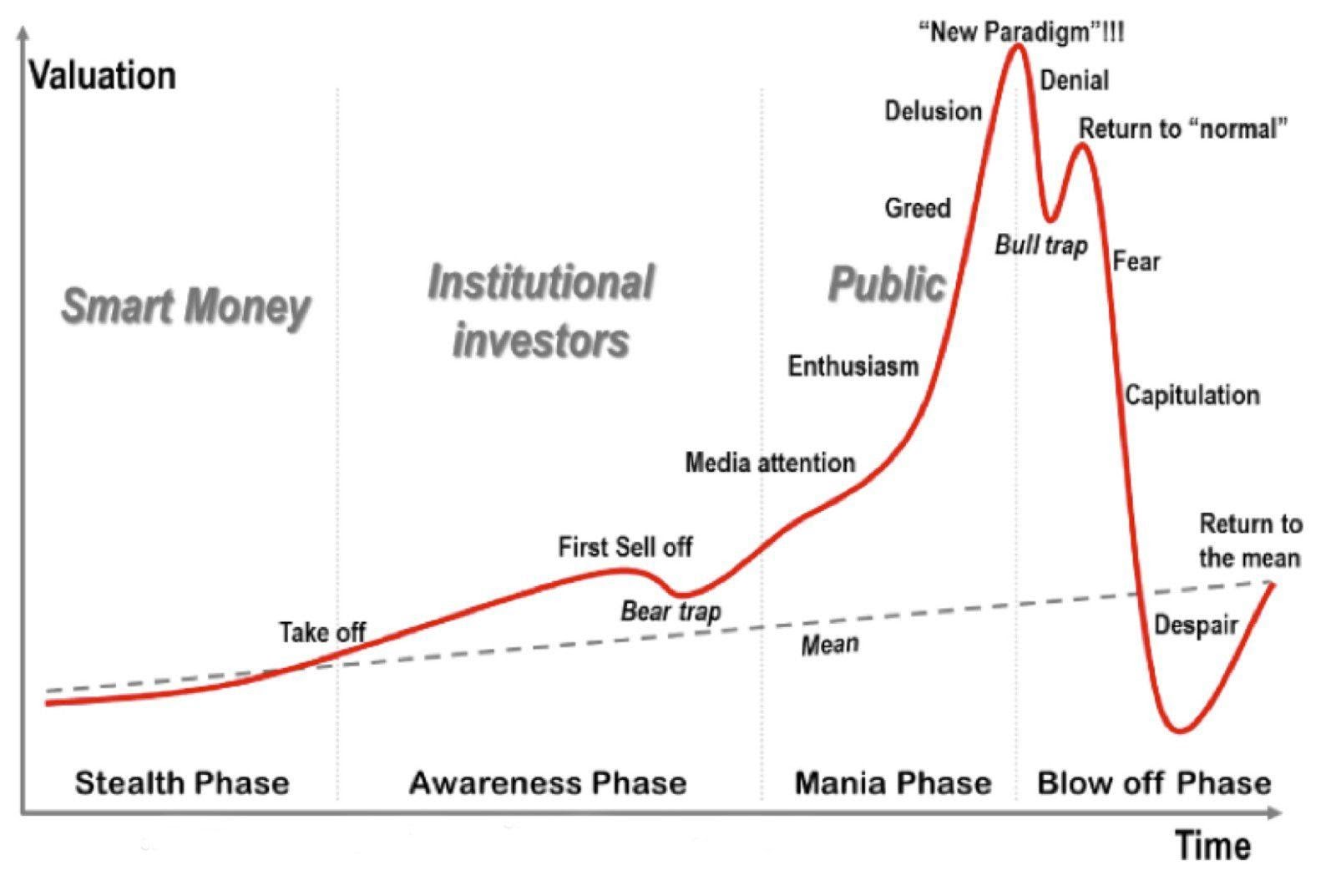

There are lots of theories about how housing bubbles — or any asset bubble — occurs. All these theories start with describing the life cycle of an investment asset and then offer various factors and triggers that prompt a bubble. Despite the variety of theories, most adhere to the theory offered by American economist, Hyman Minsky. In Minsky’s theory he offers five stages of an asset lifecycle:

1. Displacement: When investors become enamoured, like technology during the tech bubble

2. Expansion/boom: Prices rise slowly at first, then gain momentum

3. Euphoria: Caution is thrown to the wind and asset prices skyrocket

4. Realize profit: Smart money cashes out and realizes the profit

5. Panic: Asset prices reverse and investors and speculators face losses (and margin calls)

Hofstra University professor Jean-Paul Rodrigue described the phenomenon with this well-known graphic:

Are We in a Bubble?

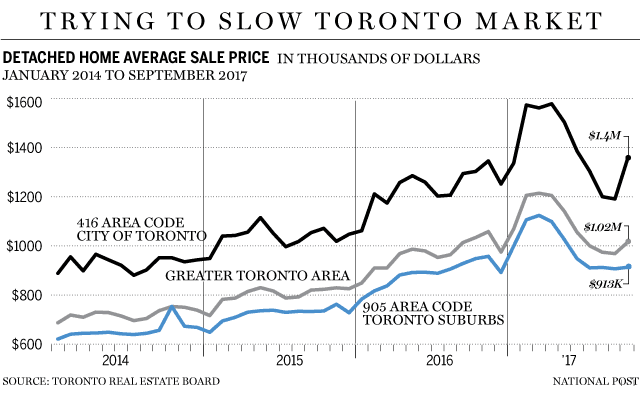

Is the Canadian real estate market in a bubble? No one will know for sure until we get a chance to view the market in hindsight. But a look at changes in the house price index for the Toronto market looks superficially a lot like Professor Rodrigue’s graphic:

As seen in the National Post chart, the rapid drop off at the end of 2018 reflects recent price declines in the Toronto market. Keep in mind, this chart (and the data from Toronto Real Estate Board) only reflects the change in listed prices, not the actual sale price. Still, even a modest drop in home values can create a substantial loss of home equity.

Mitigating Factors

Just last week, the Bank of Canada raised the overnight rate, yet again — and Canadian mortgage rates have been rising for the last year. Rising rates contribute to the unaffordability of homes. The combination of tightening interest rates and elevated home prices ends up squeezing the budget of many middle-income Canadians. Turns out home affordability deteriorated in seven out of the 10 markets measured by the Teranet-National Bank House Price Index. The national composite index shows that home prices have been outstripping income growth across the country for the last 12 consecutive months.

The Canada Mortgage and Housing Corporation’s 2018 Mortgage Consumer Survey found that the vast majority of Canadian first-time homebuyers — 85 percent — had stretched their budgets to the maximum in order to purchase their homes.

If owners are forced to sell when their five-year variable or fixed-rate mortgage term is over — primarily because they cannot qualify for a mortgage at these higher rates — then the overall market will experience a supply glut and this prompt housing price discounts.

Look at the charts and this is precisely what appears to be happening in markets like Toronto but also in Vancouver and Victoria, BC.

Enter The Mortgage “Stress Test”

Wait. The external pressures on the nation’s housing market aren’t over. On January 1, 2018, Canadian banking regulators introduced new lending rules, whereby all mortgage borrowers must qualify for the loan based on the posted 5-year fixed rate. Since the posted rate is typically 200 basis points above the discounted rates offered to borrowers by competitive lenders, this new regulation became, essentially, a nation-wide stress test.

This new “stress test” meant that approximately 10 percent of the buyers currently looking to purchase property would no longer qualify for a loan — and this reduced demand put downward pressure on the price of the supply. Worse, these new rules reduced a homebuyer’s buying power by approximately 18.5 percent — putting more demand pressure on relatively cheaper properties, such as condos and townhouses.

Still, the federal regulators argue that this stress test — a test not used in the U.S. housing market — should effectively stave off any housing market collapse in Canada. It helps build a cushion that can soften the impact of additional rate increases and help a potential housing asset bubble from metastasizing into widespread defaults, foreclosures and economic dislocation. In essence, the “stress test” may not prevent a bubble but it may help contain the damage in the event of a severe collapse in house prices.

The takeaway: While it certainly appears that Canadian real estate is working its way through the asset lifecycle, the threat of a nation-wide bubble burst seems relatively small given the strong regulations currently in place. It is, however, important to note that unlike stock prices, real estate values are ‘sticky’ on the way down. This means that current purchase or sale price is less reflective on reality since the sale of the real estate asset takes much longer than the sale of a stock. Timing markets in real estate, however, is much easier than the stock market since the volatility is lower. And, one thing we know for certain is that most of Toronto’s real estate communities are in a buyer’s market.

About the Author

Calum Ross He has funded over $2.5 billion in (6,500) mortgages since 2000, helping to create more than $1.8 billion of incremental net worth for his clients. He is the Amazon and Globe and Mail bestselling author of The Real Estate Retirement Plan. Calum is a leading authority on personal finance and investing in real estate and has spoken on stages across Canada and the U.S. He is an alumnus of Harvard Business School and holds an MBA in finance from the Schulich School of Business. He lives in Toronto.

No mortgage team in this country does luxury home financing or borrowing for wealth creation than our team. We have the business track record and formal education to support your plan and to help you achieve your financial goals. Volatile markets always create opportunities. Call our office today to discuss how we can help at 1-855-410-9905 or email ClientCare@MortgageManagement.ca.

Trust the Team Contributing in Canada’s Most Credible Media Sources