Mortgage Blog

Get the mortgage you deserve

How to make a Canadian mortgage tax deductible

November 7, 2018 | Posted by: Calum Ross

There are a lot of advantages to owning a principal residence in Canada. Property is an excellent hedge against inflation, it offers an opportunity to earn revenue from rentals (allowing the asset to act as an alternative to other fixed-income investment products) and any gain in value on your principal residence is sheltered from taxes through the federal principal residence tax exemption.

Unfortunately, there’s one big problem with buying and owning a principal residence in Canada: We don’t get to write off home mortgage interest like homeowners are able to do in the United States. That means for many Canadians, every loonie used to repay the debt (and the interest portion of that debt) is with after-tax dollars. Take one quick look at your mortgage statement and you’ll see why this is a problem. Most Canadians will spend tens-of-thousands every year paying off a debt that isn’t even tax deductible.

It doesn’t have to be that way. In fact, Canadians really can have their cake and eat it, too. Turns out, not only is it possible to shelter the profit gained on your home (principal tax exemption) but it’s also possible to turn the mortgage debt into a tax-deductible expense. This process is known as the Smith Manoeuvre, after Fraser Smith, a B.C.-based financial advisor who first put the concept on paper in the 1980s. Since its inception, the concept of capitalizing the mortgage debt to create a tax-deductible expense has taken root among investors who want to do more than save a bit towards retirement. These investors understand the importance of investing now, not just saving for later, and that means finding more ways to reduce taxes and to increase overall net worth.

Sound good? Here’s how it works:

Canada does not allow you to deduct personal mortgage interest. But it does allow you to deduct interest on loans you use for the purpose of investing.

But how do you turn your personal home loan into an investment loan? For those with large nest eggs, it may be as simple as liquidating your savings and using the money to completely pay off the mortgage on your house. Once paid off, go back to the bank and negotiate a mortgage on the home. Use this new loan to re-invest in your retirement investment plan. In the end, your monthly budget will look the same — you pay a monthly sum to pay off the mortgage debt — but now, because the loan is being used to invest (with the reasonable expectations of earning interest, dividends are appreciable gains), you are able to deduct the interest portion of your payment as a tax-deductible expense. Remember that year-end mortgage statement? The one that shows how much interest you paid in the calendar year? Well, now all that interest can be used as a way to decrease your taxable earnings. For most, that’s easily a $10,000 or more annual deduction.

But what if you can’t pay off the mortgage on your principal residence in full? Not to worry. You can implement the tax-deductible mortgage — what we like to call the “Real Wealth Accumulation Mortgage” (RWA mortgage) — a little at a time.

This time, rather than taking out a conventional loan, talk to your mortgage broker about obtaining a re-advanceable mortgage. This type of mortgage is essentially a revolving line of credit. As you pay down the principal debt, the line of credit — the amount you are allowed to borrow — increases.

To maximize the tax advantages of the RWA mortgage just make a payment towards your mortgage debt. Each payment will be deducted from the mortgage owed and added to the line of credit. Then, borrow the same sum from the line of credit and invest these proceeds in a fund or product that follows your investment strategy.

Yes, you’re still paying interest on your home mortgage. But you get a tax deduction on the interest from the line of credit — money which you use to invest. If you were to invest in dividend producing products you could also get regular cash flow from the dividends — on a favourable tax basis — that can be used to make additional payments to the mortgage, which frees up more room in the line of credit, which frees up more money to invest. And so on, and so on.

You could, of course, use non-Canadian income-generating investments, too – but you wouldn’t get the same tax break on the dividends as you do with Canada-based investments. The higher your marginal tax bracket, the more effective this RWA strategy will be for you and the greater the benefit. Why? The advantage of this wealth-building strategy is that every Loonie you pay against your mortgage principal frees up more room in the home equity line of credit, which is money that can be used to invest and the interest paid becomes a tax-deductible expense.

Why should you use a re-advanceable mortgage? Because it makes it easy and convenient. You don’t have to reapply for credit every month. You don’t have to get repeats appraisals on your home or subject yourself to any additional personal income or credit underwriting. Instead, the line of credit in a re-advanceable mortgage expands automatically as you pay down the mortgage. Just contact the lender and request the funds. As soon as you receive them, you can use the money to make the investments.

If you make bi-weekly mortgage payments, the process works even faster.

And because it’s a mortgage, ultimately secured by your home, the interest rate and terms are typically more favourable than with an unsecured loan, such as credit card cash advances and personal loans.

With a little luck, the net interest on your investments will be more than enough to cover your interest payments on the mortgage, and as you repeat the cycle, you should be able to gradually accelerate paying off your original mortgage and either increase your cash flow from the Canadian dividends or, better still, keep all your investments in the market and use the power of compounding to quickly grow your savings.

Every year, use bonuses or tax refunds to make an additional payment against your home’s mortgage. This frees up more room to invest and helps pay the mortgage off faster.

For many investors, it’s a great way to begin saving for your retirement immediately without crimping your cash flow beyond what you’re already paying on your mortgage. Of course, you can always invest more!

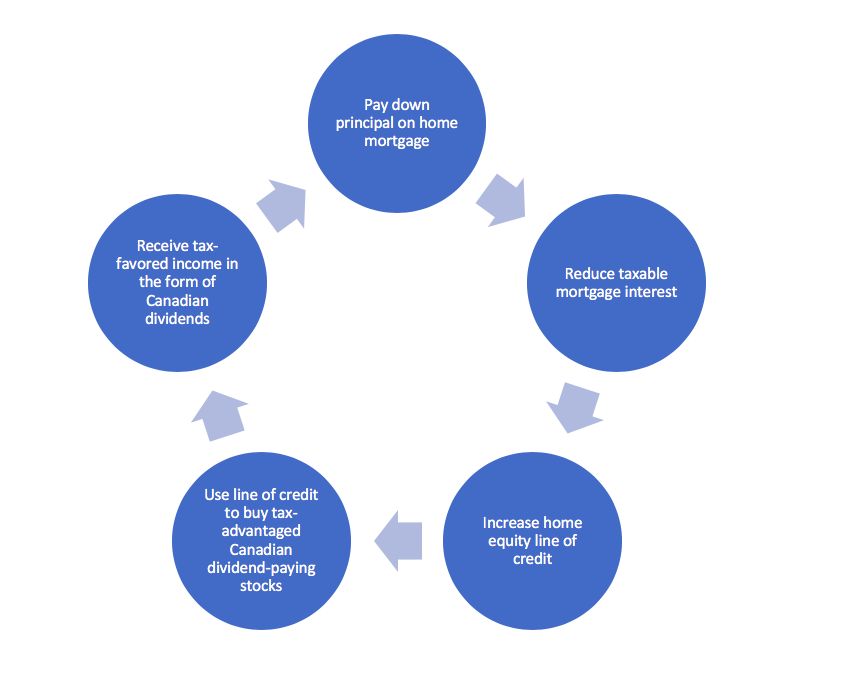

Here’s the end result:

There are a number of possible variations, but the diagram below illustrates how the cycle works, using a re-advanceable mortgage and Canadian dividend-paying stocks or funds:

The Real Wealth Accumulation strategy is very effective because long-term returns on Canadian stocks have been much greater than typical borrowing rates on home mortgages.

Of course, there are a few caveats:

The strategy works best for people with long time horizons – ideally 20 years or longer. It is probably not suitable for those with shorter time horizons who cannot ride out a significant stock market downturn.

Also, don’t let the tax tail wag the investment dog. The main benefit of the strategy is to accumulate assets. The tax benefits should be a secondary concern, and you should not take on more risk than you can handle just for the tax benefit.

Still, for those that want to accelerate their savings and build wealth, the Smith Manoeuvre strategy still offers exceptional benefits. For best results, however, you need to understand the strategy and have a solid investment plan. Where possible, seek out the advice of a qualified investment or tax professional with specific knowledge of the rules affecting the Smith Manoeuvre.

About the Author

Calum Ross He has funded over $2.5 billion in (6,500) mortgages since 2000, helping to create more than $1.8 billion of incremental net worth for his clients. He is the Amazon and Globe and Mail bestselling author of The Real Estate Retirement Plan. Calum is a leading authority on personal finance and investing in real estate and has spoken on stages across Canada and the U.S. He is an alumnus of Harvard Business School and holds an MBA in finance from the Schulich School of Business. He lives in Toronto.

No mortgage team in this country does luxury home financing or borrowing for wealth creation than our team. We have the business track record and formal education to support your plan and to help you achieve your financial goals. Volatile markets always create opportunities. Call our office today to discuss how we can help at 1-855-410-9905 or email ClientCare@MortgageManagement.ca.

Trust the Team Contributing in Canada’s Most Credible Media Sources