Mortgage Blog

Get the mortgage you deserve

Fixed vs Variable Rate Mortgages - FACT vs Fiction

June 28, 2023 | Posted by: Roar Solutions

When the prime rate is higher than fixed rates, it means that the variable mortgage rates are higher than the fixed mortgage rates. The prime rate is a benchmark interest rate that banks use to set the interest rates for their variable-rate mortgages.

Variable rates, also known as adjustable rates, fluctuate with the market interest rate, which is typically based on the prime rate. When the prime rate increases, the variable mortgage rates will also increase, resulting in higher monthly mortgage payments for borrowers with variable-rate mortgages.

On the other hand, fixed mortgage rates are set for the duration of the mortgage term, typically ranging from 6 months to more than 10 years. I have even had a ten-year mortgage myself in points because it insulated me against interest rate risk. It’s a product that many mortgage firms won’t promote because they can’t churn their book of business – which is something I don’t do unless the market justifies it. Unlike variable rates, fixed rates do not change with fluctuations in the market or the prime rate. This provides borrowers with the certainty of knowing their mortgage payments will remain the same throughout the term of their mortgage.

Lenders set fixed rates based on various factors, including the term of the mortgage, the lender's cost of funds, and market conditions. Fixed rates tend to be higher than variable rates because borrowers are paying a premium for the stability and predictability of having a consistent interest rate for the entire mortgage term.

It's important for borrowers to consider their financial goals and risk tolerance when choosing between fixed and variable mortgage rates. While fixed rates provide a sense of security, variable rates have the potential to be lower initially and fluctuate with market conditions. Borrowers who believe that interest rates may decrease in the future may prefer variable rates, while those who value stability may opt for fixed rates.

In summary, when the prime rate is higher than fixed rates, it means that variable mortgage rates are higher than fixed rates. Variable rates fluctuate with the market interest rate, while fixed rates remain the same for the duration of the mortgage term. The decision between fixed and variable rates depends on the borrower's financial goals and risk tolerance.

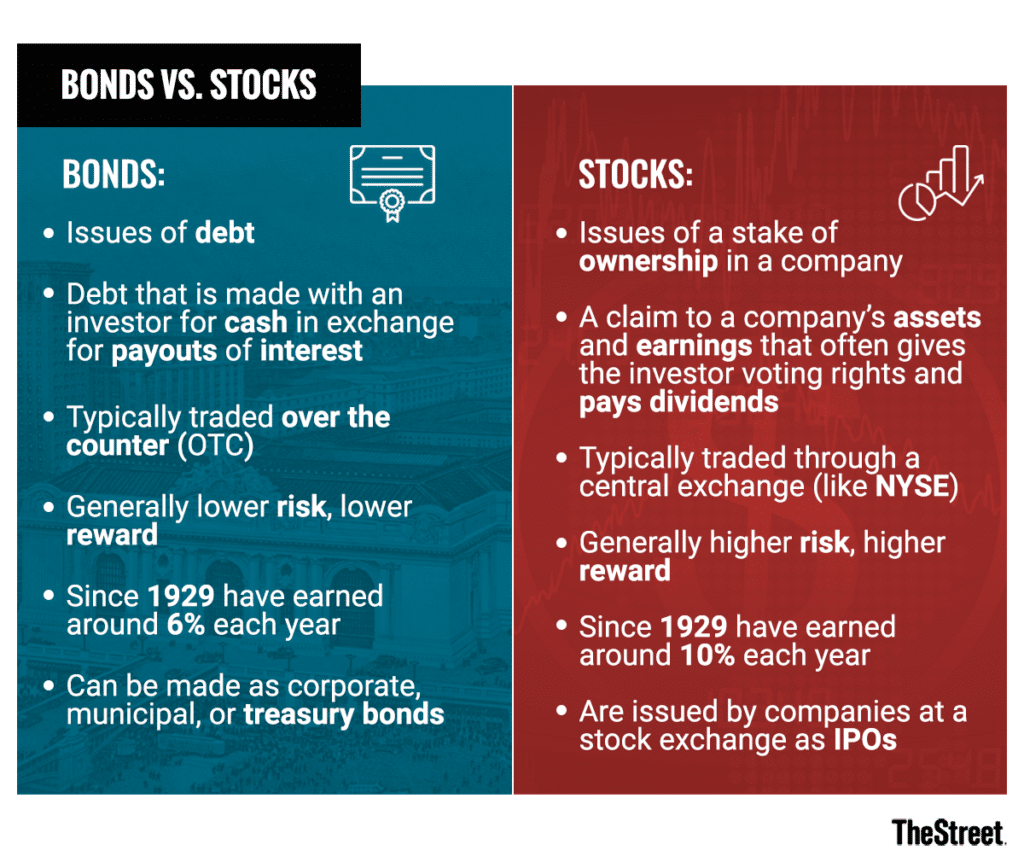

Typically, when stock markets decline, we also see a decrease in mortgage rates (and vice versa), and many ask the question, “Why does this happen?”. The key thing to keep in mind for mortgage consumers or bond market investors is that bond (debt) markets and stock (equity) markets basically compete for investment dollars at any given point in time. For this reason, a bullish (positive or strong) equity market would pull investors’ funds (which are limited) away from the bond (debt) markets and see them redeployed into stock (equity) capital markets. Conversely, when the stock markets are decreasing in value this is often caused by a sell-off and much of the funds from that sale go into bond markets.

When money is flowing from stocks toward the bond markets, this increases the demand for bonds and the sellers of these bonds (both government and corporate bonds) subsequently have their face values go up while driving yields down. Please also keep in mind that when bond prices go down – bond yields go up. This can be more simply explained if you look at the fact that that bonds trade at a discount to the face value of the bond and consider that the return investors earn is comprised typically of the coupon rate and the difference between the market price and face value of the bond. The larger the discount from face value, the greater the yield to maturity for the investor – therefore the investor yield goes up as the price of the bond goes down. It is this increase in yield that ultimately attracts investors back into investing in bonds when equities rise. Investors simply seek the most effective (risk-adjusted) home for their investment dollars. If this seems complicated to you then you are not alone. For a more detailed overview try the Bond section of Investopedia: https://www.investopedia.com/terms/b/bond.asp

Essentially – what we see in short-term market dynamics is when stock indexes fall, they in turn push bond prices higher and thus bond yields lower (all else equal). It is for this reason that we often see a quick rally in the stock market push up the yields on mortgage rates – at least in the short term. Since the Canadian bond market is closely correlated with the US bond market – falling yields south of the border often put downward pressure on our bond yields and thus lower fixed mortgage rates here in Canada.

I would like to quickly point out that there is a plethora of other market dynamics in play at any given time. While much of macro and microeconomic theory is predicated on a concept called “ceteris paribus” which is a Latin phrase meaning “other things remaining equal” … we all know other things don’t remain equal in the real world. Monetary policy, fiscal policy, inflation, and geo-political economics or virus outbreaks are always at play at varying levels of relevance.

Trust the Team Contributing in Canada’s Most Credible Media Sources